Internal audit performance

A summary of external quality assessment (EQA) reviews of internal audit functions undertaken in 2022/2023

Internal auditors will not be surprised that permacrisis, an extended period of instability and insecurity, was the word of the year in 2022 according to the Collins and Oxford dictionaries. Signalling yet further challenge, the World Economic Forum 2023 Global Risks Report talks about a future with polycrisis, a cluster of related risks with compounding effects, such that the overall impact exceeds the sum of each part.

Internal audit must be flexible, collaborative, proactive and risk aware to be relevant in an environment of constant change. With few exceptions, there is general conformance with current Standards (IPPF 2017) and maturity ratings of excellent were achieved by some functions which is an impressive result. However, our results this year show that there is improvement required across all areas with two notable findings.

Firstly, now is the time to move away from the traditional annual plan to a more dynamic, flexible plan of work. And secondly, that the majority of our EQAs identified opportunities to coordinate assurance across the three lines model, maximising benefit for the organisation and eliminating inefficiency.

Our results this year show a reduction in conformance with the 1300 series regarding quality and improvement. As you read this report, please take time to reflect on the insights to create or add to your own programme. Continuous improvement is vital to our profession.

Download the report (pdf)

Key takeaways for 2022/2023

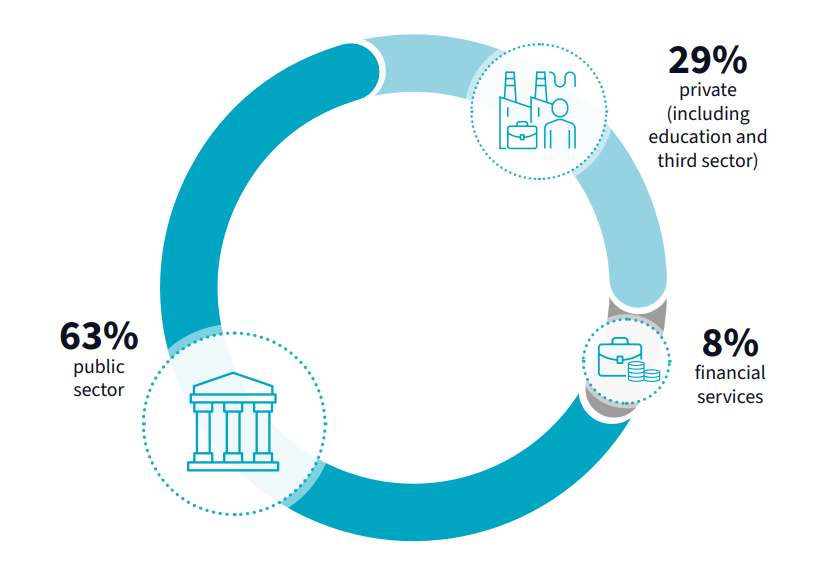

Here is our breakdown of reviews for 2022/2023.

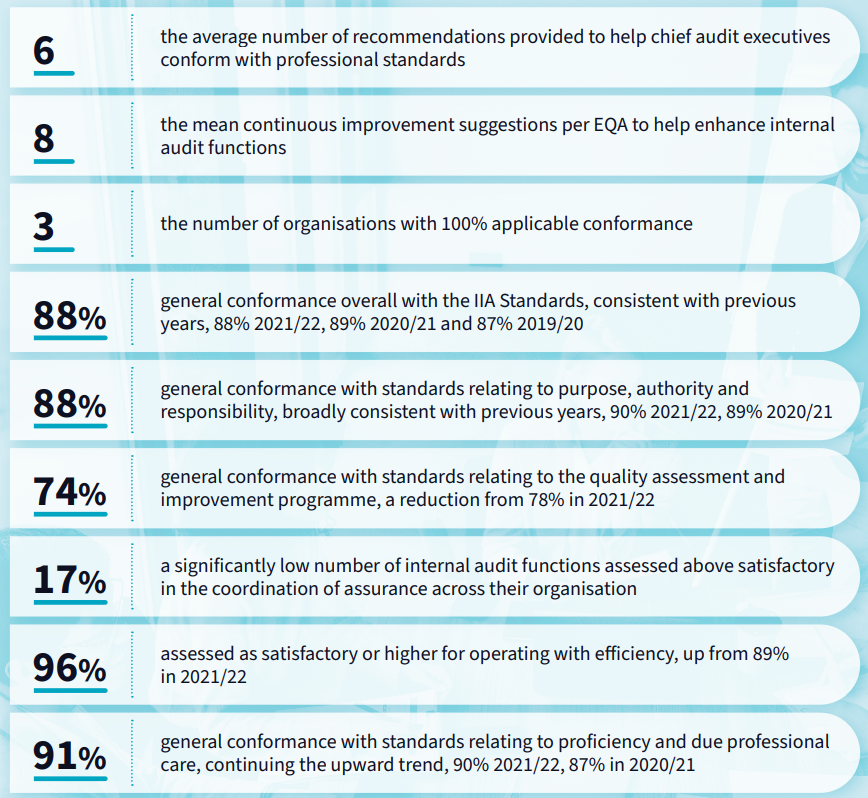

The findings of these reviews are summarised as follows:

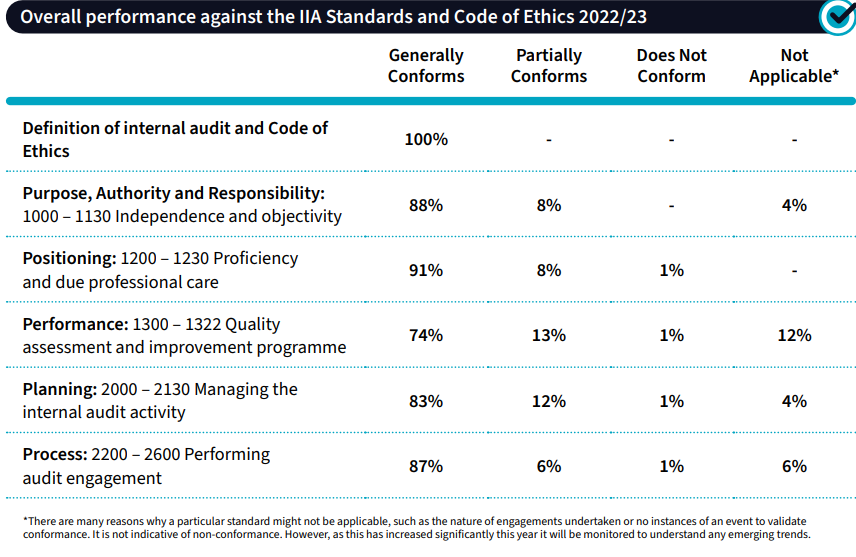

Overall performance against IIA Standards

We note that overall conformance with the Standards has improved over the last three years. In particular, it’s encouraging to see the levels being attained in the performance standards, relating to the fundamentals of doing the job.

The following table summarises performance against the Standards and Code of Ethics in the period 2022 /2023 and is a useful benchmarking tool when completing your own self-assessment.

Internal audit’s credibility and relevance is fragile. With so much uncertainty and volatility in the risk landscape, it will take effort to maintain and that is where the value of internal and external quality assessments come to the fore. CAEs with a commitment to continual learning and improvement gain trust from governance leaders and inspire their teams to perform at the highest levels.

Access previous reports

2021-2022 Internal audit performance report

2020-2021 Internal audit performance report

2019-2020 Internal audit performance report