Local Authority Internal Audit Virtual Forum

20 January 2021

Please note:

- All Institute responses are boxed and highlighted blue

- Where the Chair comments in that capacity, the box is highlighted in yellow

- For confidentiality, the identities of all delegates/attendees are anonymised

CEO welcomeThank you for joining us for our session on the HIA annual opinion. Our speakers today are Ruth Powell and Cllr Lynne Brooks. Ruth is Head of Internal Audit for Lancashire County Council and Lynne is Chair of the Audit Committee for Mole Valley District Council. We are also joined by Liz Sandwith, the Institute’s Chief Professional Practices Advisor, Derek Jamieson, Regional Director for the Institute, and our chair Piyush Fatania, Head of Audit, Risk, Assurance and Insurance Services, Gloucestershire County Council, and a member of the Institute’s Council. |

Chair's opening commentsWelcome to our Local Authority Virtual Forum. This has been a far from usual year which presents us all with the challenge of how to provide a meaningful level of assurance in our annual opinion based on the work we’ve undertaken and the assurances we’ve received. Our first speaker today will be talking about the basis on which we can provide the assurance this year and our second speaker will discuss the Audit Committee’s expectations around the level of assurance. |

Key takeaways

During the discussion many delegates expressed interest in receiving a copy of the 'year end self-assessment checklist' that some members use. Click here for a generic template for you to adapt and use.

1st Speaker

- Having done very little audit work, and with the organisation not having had much capacity to be audited, the audit team have been redeployed.

- It is, however, possible to give a positive favourable audit opinion based on work undertaken over the past few years and other sources of intelligence and assurance.

- Over the last few years there has been a lot of change and improvement which has led to a level of comfort that the organisation is adequately governed, risks are managed and that there is a reasonably good framework of control – both in terms of business as usual and the response to COVID-19.

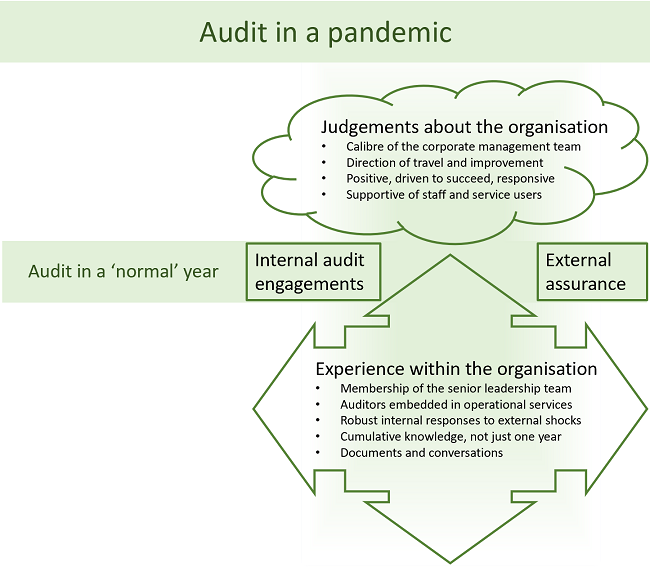

- In a normal year, the opinion would be based on the completion of the audit plan and other external assurance.

- This year, the evidence has come from elsewhere including judgements about the organisation and experience within it – as demonstrated in the infographic below.

- This has provided a lot of information and evidence in addition to the minimal audit programme that has been delivered.

- Some specific audit work has been undertaken on decision-making which underpins this additional information and will be key to the opinion given.

2nd Speaker

2nd Speaker

- As an Audit Committee Chair, building a relationship with the internal auditor and gaining confidence has provided the ability to look beyond reports and look in depth at the day-to-day issues.

- However, in the current context, will the same internal auditor be able to provide the same level of confidence and assurance without access to papers, some officers, and staff in order to give an unqualified opinion.

- In some cases, internal audit might be seen as a secondary requirement, a distraction or even a negative management process.

- How have procedural changes and revised working practices affected day-day services and how have the internal auditors picked these up to give suitable assurance?

- Can the Audit Committee Chair retain the necessary confidence in the assurance given in the annual opinion?

- The role of internal audit is an effective part of setting the council’s culture, its commitment to good governance and in setting the tone and quality expected.

- This is not just in local government but also extends to a business environment.

- The HIA should comment in their annual opinion on whether this culture has changed as a result of COVID-19 and if so, why it has changed.

- Two questions for HIAs: -

- Is it credible or possible to give an unqualified opinion for 2020/21 and what impact will that have on 2021/22 workload?

- Will internal audit costs need to increase as has happened with external audit? If so, what do audit committees need to do to prepare for this?

Comment from CIPFA

- CIPFA acknowledge that this has been a difficult year which has presented some unique challenges. What we do this year will be different to previous years, but we would encourage HIAs to: -

- Think widely and creatively about where you can get wider assurance including both additional sources and what was done in previous years.

- Bear in mind that the value of independent assurance is what internal audit brings over and above all other sources of assurance and that shouldn’t be devalued.

- Write your opinion in a way that is most meaningful for your audit committee and leadership team, that clearly communicates the basis for the opinion and the sources used.

- It is very important to be responsive to the challenges of the organisation and think creatively in what can support the opinion. The test is whether you have 'sufficient, reliable, relevant and useful information' as per PSIAS.

Chair's closing commentsToday, we have heard from two great speakers who have given us a lot to think about in terms of how to provide our opinion and the challenges that we might face – particularly from audit committees. It is important this year to stand firm and demonstrate that the work we have done this year can be used to shape an opinion. Also, whilst we can provide a level of assurance, the challenge of audit committees is likely to be higher than usual. We need to be having conversations with our chairs and asking them how we can best demonstrate to the committee that the level of assurance we can provide is acceptable and reliable. Finally, internal audit responds to the risks and activities of our councils which have changed over the past years. Internal audit has responded remarkably and helped our councils to provide their services. |

Institute's commentsThis is an important and timely subject – as shown in the level of debate at the meeting. As well as presenting real challenges, it also provides opportunities for internal auditors to think creatively about how they can provide real value to their organisations.

During our earlier forums many of you shared your recent experiences, including some great solutions to the challenges that the pandemic has presented. We would actively encourage you to enter our 2021 Audit & Risk Awards. There are five categories to choose from and deadlines for nominations closes on Friday 29 January 2021. For more details, click here. Our next LA Forum meeting, 17 February 2021, will focus on independence and objectivity. A particularly relevant discussion in these times of being increasingly asked to cover more ground with decreasing resources. Thank you for attending. As always if you have any ideas or suggestions for what we might include in future agendas please contact Liz Sandwith liz.sandwith@iia.org.uk |

Chat box comments

- I think part of the challenge has been around getting engagement for real time assurance - simply being in the loop with key decisions. This is the best way to minimise drain on officer time and to get assurance over the organisation's approach. This has been partly successful - but the size of the organisation makes it difficult.

- We have used the IASAB guidance which was issued in May on the role of IA in the pandemic within the opinion and providing narrative against all of the bullet points in terms of how the service has been delivered differently – particularly in the first quarter of the year.

- The key in working effectively with audit committee chairs and avoiding any pushback has been to engage with them throughout, taking a pragmatic approach and regularly revisiting risk assessments.

- In considering this year’s opinion, we have a strategic 3–5-year plan as it irons out some peaks and troughs. This enables this year’s opinion to draw upon assurance from previous years.

- Considering governance from the top-down, committees and cabinet seem to be operating very well remotely. Risk management is strong in my council and the corporate board has not been restricted. We ask the directors to check and sign a governance self-assessment/checklist which includes an assessment of compliance as well as whether that has changed in the past year.

- I have re-prioritised my audit plans for the three authorities I manage with greater focus on key financials and the very high-risk audits remaining in the plans. We have had support from all management teams and Audit Committees to complete this work. I do still plan to refer to alternative sources to bolster my annual opinion as well.

Chat box Q&A

Q What is the view of external auditors to the approach to providing an opinion in a pandemic?

A From previous experience and for this year, the key consideration for external auditors is that there is an internal audit function doing the work. The team is coming back together after redeployment after Easter which will give them some comfort going forwards.

Q Will you be including or acknowledging any limitations of scope within your opinion?

A The opinion will include a narrative on the basis of the opinion but if possible, it will not include any specific limitation.

Q I agree on the approach – this is a really good opportunity for internal audit to demonstrate our ability to be flexible and responsive to current issues and finding a solution. We need to be careful with the opinion if audit staff have been redeployed - an 'accepted' opinion could lead on to the question of "do you need the resources?"

A Although our annual opinion is key, it has not always been a requirement and the value in internal audit comes not only from the opinion but in the work leading up to it. Our resources are not just geared up to providing the opinion.

Q As a chair of an audit committee, is the ability of internal auditors to use free text to phrase their opinions helpful? Or would you prefer some form of standardised wording that would give a more consistent and comparable view?

A In normal circumstances, free text would be preferable. However, in the current COVID-19 context, having some standard wording to enable comparisons across the sector would be extremely helpful in providing additional guidance and comfort.