New Standards - the IPPF evolution 2023

NEW IPPF and GLOBAL INTERNAL AUDIT STANDARDS

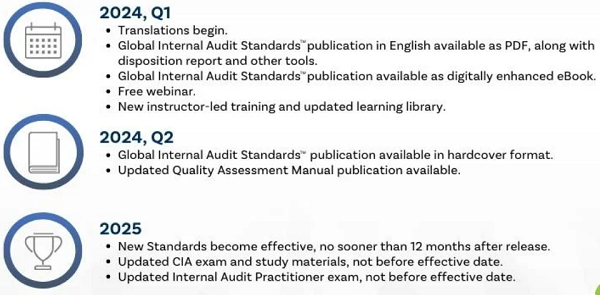

Effective date for conformance 9 January 2025

Click here for the printable pdf version of the new Global Internal Audit Standards

- Condensed version of mandatory elements

- Two-way mapping document - 2017 to 2024 Standards and back again

- Copyright notice

1. ACTION all - Free webinar on demand

Get to Know the New Global Internal Audit Standards - click here

- Understand the structure of the new IPPF and Global Internal Audit Standards.

- Learn about the primary changes between the 2017 Standards and the new Standards.

- Become familiar with the content in each section of the new Standards.

- Hear about how the new Standards will affect internal auditors and internal audit functions.

2. ACTION CAEs - discuss Domain III with Audit Committee.

This document helps clarify and raise awareness of the audit committee's governance roles and responsibilities as set out in the new Standards, including the information that should be provided by the chief audit executive.

Governing the internal audit function

3. ACTION all - read feature in Audit & Risk Magazine.

An insightful feature focusing on how the new Standards raise the bar for the profession.

"Now more than ever, [internal auditors] need standards that meet their needs and raise the quality of the internal audit services they provide" Mike Peppers, International Internal Audit Standards Board (IIASB) immediate past Chairman.

The new Standards articulate the keys to effective internal auditing by grouping the Standards into five domains:

• Domain I: Purpose of Internal Auditing

• Domain II: Ethics and Professionalism

• Domain III: Governing the Internal Audit Function

• Domain IV: Managing the Internal Audit Function

• Domain V: Performing Internal Audit Services

The IPPF structure has also changed.

Mandatory topical guidance on subjects such as cyber will also be published - we will keep you updated on progress.

![]()

The process is being led by Global IIA, click here for full details, including a video from President, Anthony Pugliese.

Background

The 2024 IPPF including new Standards is the result of a multiyear project, extensive consultation process and listening to members.

Updating standards for a changing world

Short insightful paper, useful to share with your Audit Committee, senior leadership team, CEO.

Public sector briefing

Two page overview of proposed changes specific to public sector requirements (US language but relevant message).

Click here to watch short videos explaining each new domain (proposed version of new Standards)

Topical Requirements (tbd) - these will support the Standards. Eight topics are under consideration. Specific to audit engagements they will introduce mandatory elements to ensure the quality and consistency of methodology worldwide - read more here.

Copyright notice

The IIA retains sole copyright to the IIA materials in any form. Permission to use is granted exclusively for: (i) an individual user’s internal use or (ii) an organization’s internal use. Insubstantial portions of materials may be used by the individual or organization internally only for inclusion in its internal audit documentation, systems, training materials, and other related documents. IIA materials may be included in any individual file to the extent that such storage is not further limited or prohibited by supplemental terms for the specific materials. For any other use, permission or license maybe required; for questions, contact permissions@theiia.org.